With the surge in real estate prices, you may find it difficult to align your closing dates because homes are selling so fast. Because of this, more people have been getting a bridge loan. Take a look at how you can use bridge financing to help with this problem.

What is bridge financing?

A bridge loan, also known as bridge financing, is a temporary loan that allows you to use the equity of your present home to pay the down payment of your next home even before your home sells. It is commonly used when closing dates are not aligned and you are in a competitive housing market with high demand. This loan is a quick and easy solution if you are financially stable.

These loans are usually between 3 to 6 months and can go up to 12 months, depending on your financial circumstances. A stable income and a good credit score are necessary to be eligible for this loan. The majority of lenders also need a minimum of 20% equity. However, some lenders will consider your income level and adjust the requirements accordingly. After those qualifications are met, you must make a sale agreement on your current home that contains the firm closing date and a purchase agreement on your new home in order to get a bridge loan.

The cost of bridge financing

While this loan is convenient and can provide comfort, there is a cost associated with this loan.

The cost mainly consists of three values:

- Legal cost- Registering the loan requires your lawyer to do extra work so that they may charge more

- Lender fee- Lenders need to set up the loan so that they can charge for the time it takes them to set it up

- Interest rate- The bridge loan interest rate in Canada will approximately be Prime +2.00% or Prime +3.00%

To sum up the costs, a bridge loan usually costs between $1000 – $2000, but it also depends on a case-by-case basis and your circumstances.

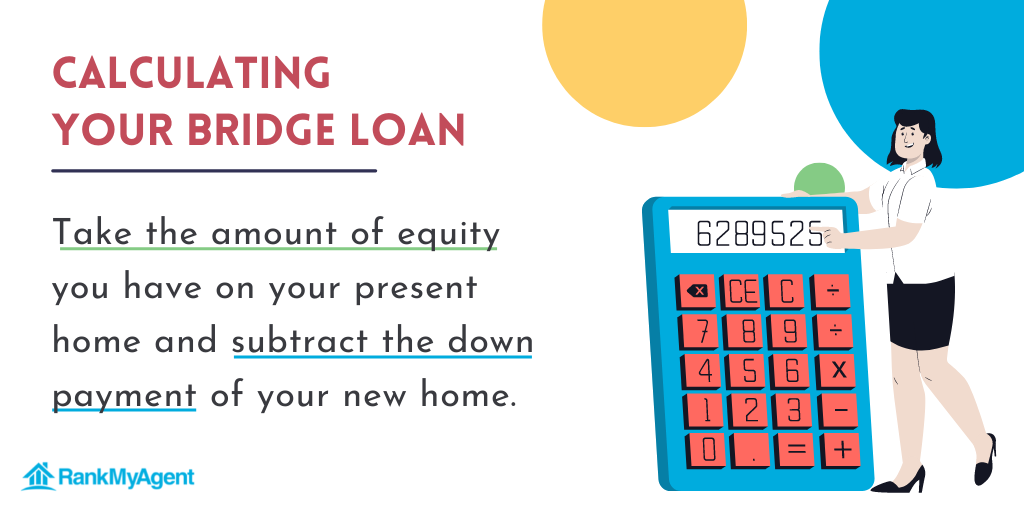

Calculating your bridge loan

Now that we’ve looked at the cost of a bridge loan, how much can you get from a bridge loan?

To calculate your loan, take the amount of equity you have on your present home and subtract the down payment of your new home. Let’s take a look at a bridge loan example.

You have $150,000 equity on your present home, and your down payment for your new home is $50,000.

$150,000 – $50,000 = $100,000

Your bridge loan is $100,000 and is financed until the sale of your present home is over.

To get an accurate estimate of the sale amount available for your bridge loan and the approximate cost of your loan, be sure to use a bridge loan calculator.

Pros of bridge financing

Now that you know what a bridge loan is, let’s look at its advantages.

Buy your next home before the current one sells: The main advantage of this loan is that you get to buy your dream house even before your current home sells. This provides relief as you don’t have to stress over your home not being sold in time for purchasing your next home, especially if you are in a competitive area.

Financial Flexibility: A bridge loan also provides financial flexibility as it allows you to use the equity of your present home to pay for the down payment of your new home. If you find a house you love but can’t afford the down payment of it, this loan can be useful in covering the balance until the sale of your present home closes.

Find capital for renovations: if you want to make changes or renovations to your new home, this loan provides you with the funds and extra time that may be needed before you move in.

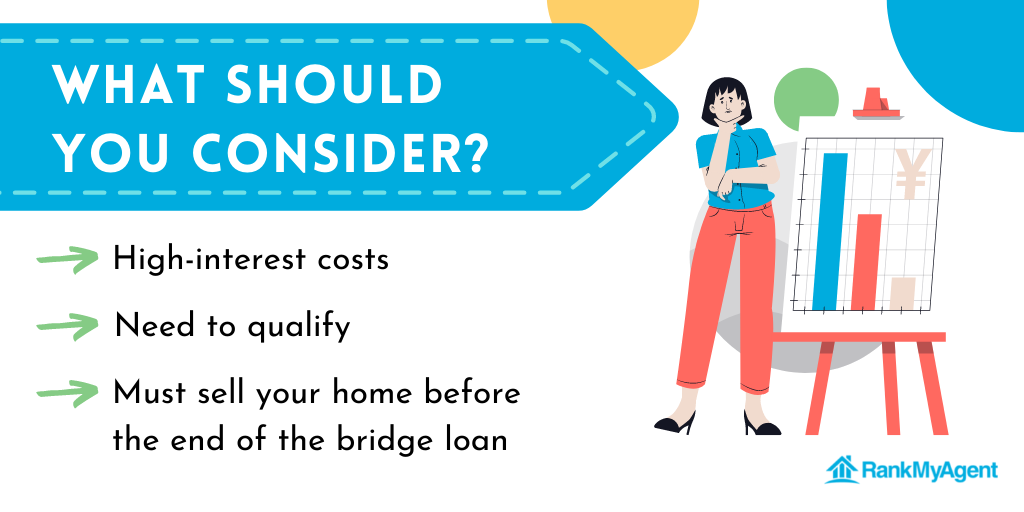

Cons of bridge financing

Despite how efficient bridge financing may sound, there are possible disadvantages that you should consider.

High-interest costs: Even though this is a short-term loan, the interest can get costly as the interest rates are generally higher than the interest rate you are paying for your mortgage. So evidently, the longer your loan is, the more interest you will have to pay your lender.

Need to qualify: Various factors, including income, credit score, and equity, determine the terms of your bridge loan. So, many aspects of a bridge loan may fluctuate, like the duration of the loan, interest rate, and requirements.

You must sell your home before the end of the bridge loan: This loan can lead to a higher risk because if your bridge loan exceeds the term and your present home is still not sold, you will have to pay for two mortgages until you can sell your home.

Who offers bridge loans?

Since more homeowners are using bridge loans, the well-known banks, including RBC, Scotiabank, BMO, CIBC, and TD, all provide their mortgage customers with the option to get a bridge loan. However, you can always reach out to your mortgage broker for more options if you’re unsure whether your bank offers bridge loans. A mortgage broker can help you find alternative lenders who may be more flexible towards home buyers with low credit scores or inconsistent incomes.

Alternatives to bridge loans

The most common alternative is the home equity line of credit (HELOC), also known as a second mortgage, which allows you to borrow against the equity in your house. The lender will then use your home as collateral to guarantee that you will pay back your loan. This is very similar to a bridge loan, except the repayment period can be as long as 10 years later.

If you have a stable job and a good credit score, another alternative is a personal loan which doesn’t require collateral and is usually funded more quickly. Certain lenders can give you a decent-sized loan with lower interest rates and fees. However, if your credit score is not superb, you can still qualify for a personal loan, but it may have higher interest rates and more fees.

Overall, bridge financing is a great resource if your closing dates don’t match up. However, you should contact your mortgage broker to find out the pros and cons that specifically apply to you.

{kind=link}