A down payment is typically (and ideally) at least 20% of the full price of a home. To most Canadians, this is a lot of money, especially with home prices sky-high. Luckily, the government, over the years, have developed tools to help first-time homebuyers make the largest purchase of their life.

In this article, we explain these tools and look at how they can help you buy a home. The tools include the Home Buyers’ Plan, the new First-Time Homebuyers’ Incentive, and the various tax rebates and credits available to first-time homebuyers.

Home Buyers’ Plan: Borrowing from your RRSP

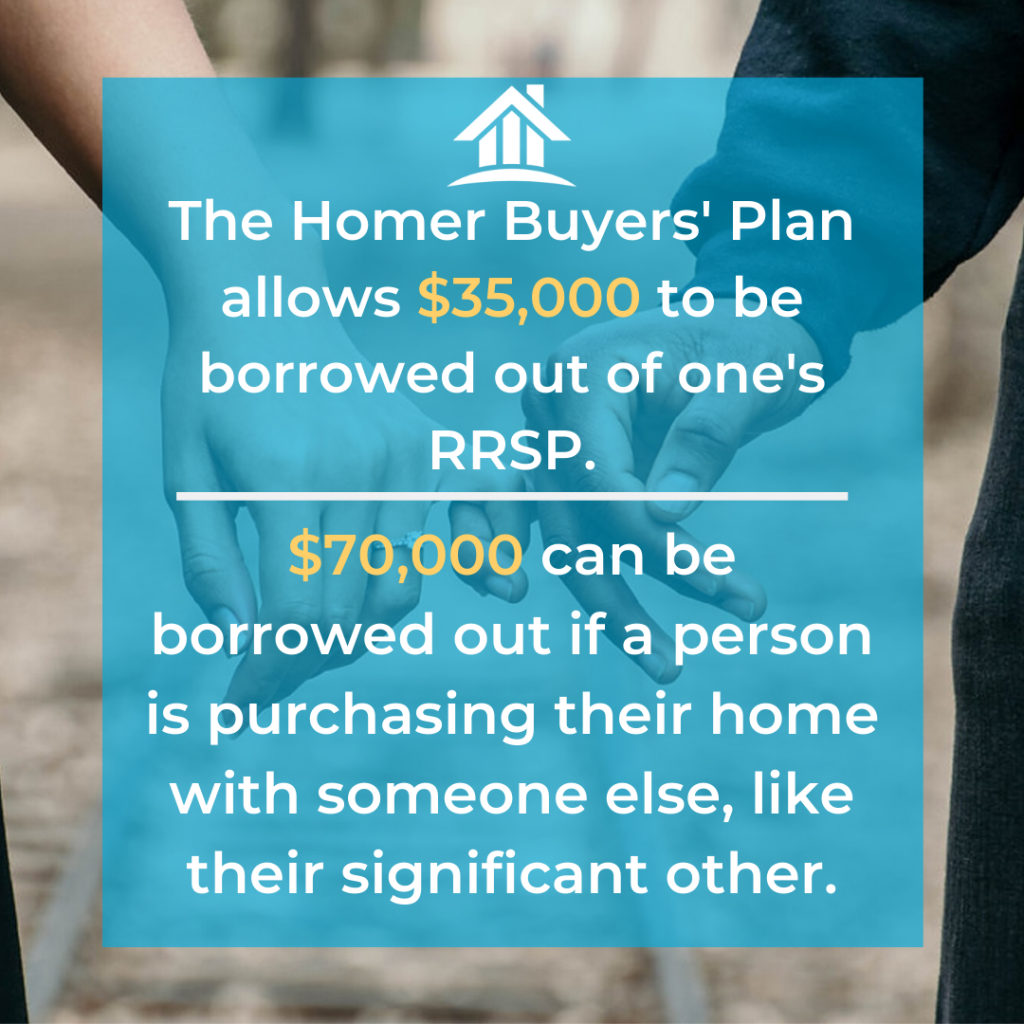

The Home Buyers’ Plan lets any first-time homebuyer buying or building a home to borrow up to $35,000 from their Registered Retirement Savings Plan (RRSP). This amount used to be $25,000 until March 19, 2019, when it was raised to $35,000. If you’re purchasing your home with someone else, like a significant other, each person can use the Home Buyers’ Plan for a total of $70,000.

Although it mentions “first-time” homebuyers, if you’ve previously participated in the plan, you may be able to do it again if your borrowing balance is 0 as of January 1st of the year. Just remember that every year that the money isn’t in your RRSP is another year that it’s not growing. Without the help of this appreciation, it could impact what you have ready for retirement.

Although withdrawing this money is tax-free, it has to be repaid within 15 years to remain so. The repayment period starts the second year after the year that the money is withdrawn. So funds withdrawn in 2019 have 2021 as the first year of repayment. The tax consequences of not paying back the loan within the allotted time could result in a hefty income tax.

Unlike mortgages and other loans, there are no consequences for paying back the money early.

First-Time Homebuyer Incentive: Sharing Equity with the Government

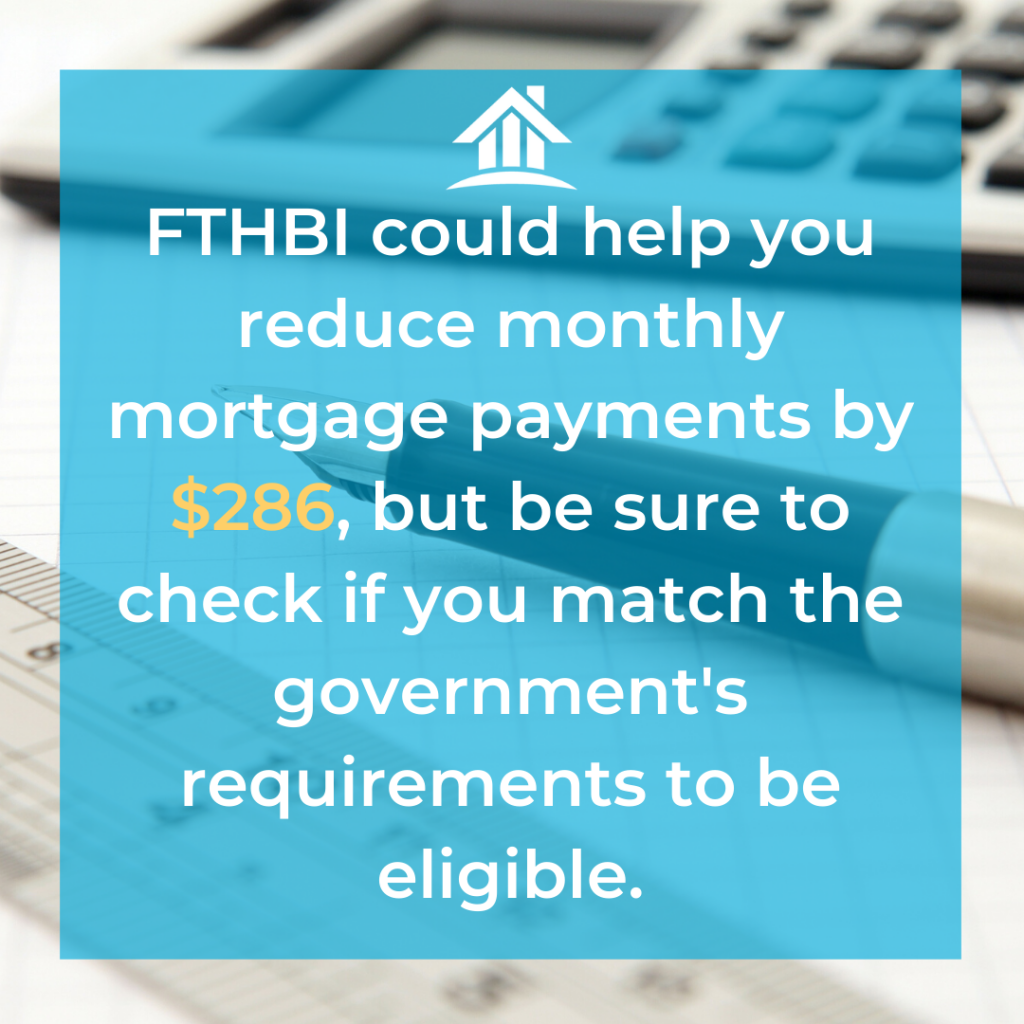

The First-Time Homebuyer Incentive (FTHBI) started on September 2nd, 2019 as part of the government’s national housing strategy. It’s expected to help Canadians fitting into a specific criterion reduce monthly mortgage payments by $286.

The government does this through a shared-equity mortgage program, where they provide a first-time homebuyer with 10% of the purchase price of a new home, or 5% of a resale home. This capital comes interest-free because it is not a loan. The government is actually purchasing part of the equity.

When the property is sold or after 25 years, the homebuyer must pay back either 10% or 5% of the home’s current market value. Thus, if the home declined in value, the homeowner pays back less than what they got. If the home’s value appreciated, they must pay back more.

For example, a homebuyer purchases a $100,000 new home and receives $10,000 (10%) from the FTHBI. If the home appreciates to $400,000 after 25 years or when they sell, they’ll have to pay back $40,000—10% of the market value after 25 years or at the time of the sale. One big benefit is that this amount can be paid back at any time, meaning you could pay it back when the property market is weaker to maximize the benefit.

As great as it sounds, there are severe limitations to this tool. To qualify for FTHBI, homebuyers must have a combined household income of $120,000 or less. The price of the mortgage plus the incentive amount also cannot exceed more than four times the buyers’ household income. This effectively limits the maximum purchase price of a qualified home to around $500,000. This likely rules out Vancouver or Toronto purchases, as even most condos in these cities have surpassed this maximum purchase price.

Another drawback of the program is that homebuyers using the plan with less than a 20% downpayment still need mortgage default insurance. If you have 10% of the purchase price ready and hope to get another 10% from FTHBI, this won’t help you wiggle your way out of default insurance. The FTHBI is almost like a second mortgage on your home—not part of your down payment.

Tax Rebates and Credits

In addition to tools that can help you get the money you need for a down payment or to reduce monthly mortgage payments, multiple tax rebates and credits can help avoid some of the costs of purchasing your first home.

First-Time Home Buyers’ Tax Credit

The First-Time Home Buyers’ Tax Credit came into effect in 2009. It provides a $5,000 non-refundable tax credit if you and the home you’re buying fit a certain criterion. The credit works out to a maximum of $750 back in your pocket.

To qualify, you and your spouse/common-law partner need to buy a qualifying home and must also have not lived in another home owned by you or your partner in the past four years. You and your partner also get a combined total of $5,000 tax credits. This means that regardless of whether it’s a solo or joint purchase, the maximum tax credit is $5,000.

HST/GST Rebate

The HST/GST housing rebate allows a homeowner to recover the GST or federal portion of HST from the purchase of their home or from any renovations that they made to it. To qualify, this home must be your primary place of residence, among other conditions. Depending on your province, the PST or provincial portion of the HST may also be recoverable.

Land Transfer Tax Rebate

If you’re a first-time homebuyer purchasing a home in British Columbia, Ontario, or Prince Edward Island, you could also recover some or all of the land transfer tax paid on your purchase. The recoverable amount depends on the specific province. The City of Toronto also provides a rebate on the city’s land transfer tax, in addition to the provincial one. The qualifications for each rebate differ depending on the province and whether you’re purchasing in the City of Toronto.

As a first-time

homebuyer, many tools can help you purchase your first home. You can borrow

from your RRSP through the Home Buyers’ Plan, split the equity of your home

with the government via First-Time Homebuyer Incentive, or recover some money

through various tax credits and rebates. Make sure to speak to an accountant

and your realtor to make the best use of these tools.

{kind=link}